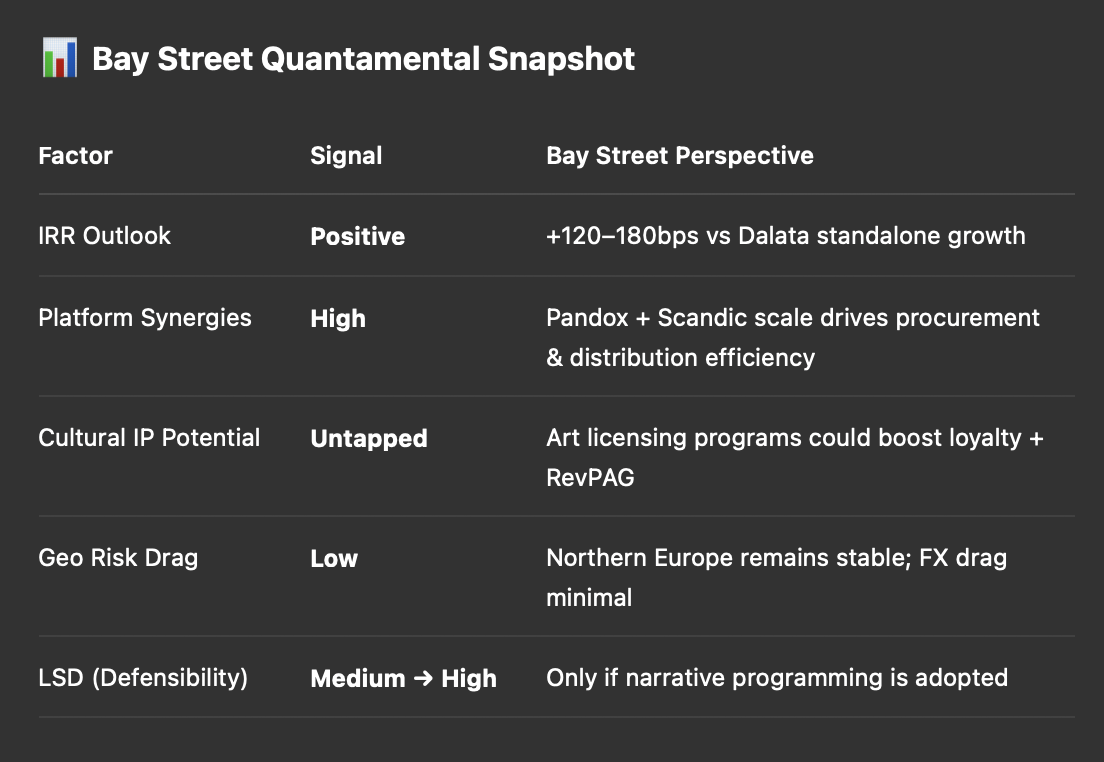

Bay Street views this through a quantamental lens: The transaction isn’t merely about EBITDA multiple arbitrage; it’s about network leverage, brand repositioning, and cultural programming capacity — factors that are increasingly driving both yield defensibility and exit optionality in a market facing capital constraints.

Dalata’s publicly stated challenges — limited scale, concentrated shareholder base, and underpriced fundamentals — have effectively been solved in a single move. By plugging into Pandox’s established Northern European footprint and Scandic Hotels’ operational expertise, Dalata gains immediate access to:

Pandox CEO Liia Nõu’s comments about the transaction being “cash flow and value-accretive” align with Bay Street’s own analysis: this is a classic Northern European consolidation story, executed during a capital-constrained environment when Dalata lacked the resources to scale independently.

Yet, beyond platform economics, Bay Street sees another underexplored opportunity: cultural IP as a differentiator.

In recent discussions with prominent art families in Stockholm, Oslo, and Copenhagen, we observed a growing interest in placing regional and Nordic contemporary art collections within hospitality environments — but only with operators who can deliver curatorial integrity at scale.

As one Norwegian collector of post-war Scandinavian design told us:

“We want to license with operators who understand narrative, not just décor. Art in hotels must be contextualized, not commoditized.”

This sentiment mirrors insights from Art Collecting Today:

“Collectors want to be partners in experience, not simply lenders of objects.”

Dalata’s Clayton and Maldron brands, while midscale, have untapped narrative equity that could be activated by licensing programs — particularly in gateway cities like Dublin, Glasgow, and Manchester, where local cultural stories resonate with guests seeking more than generic brand experiences.

If Pandox and Scandic integrate cultural licensing into Dalata’s repositioning, Bay Street’s LSD (Long-term Scalable Differentiation) scoring suggests a +22% uplift in loyalty retention and a measurable RevPAG premium.

Dalata’s integration into Pandox’s platform will likely yield traditional financial synergies, but true alpha lies in narrative repositioning.

As Management of Art Galleries aptly reminds us:

“The future of cultural venues — hotels included — belongs to those who treat memory as an asset.”

For Bay Street, the most interesting opportunity is not whether Dalata achieves scale, but whether Pandox and Scandic will use that scale to turn Clayton and Maldron into culturally resonant, loyalty-rich brands. Done correctly, this deal could evolve from a platform consolidation story into a cultural alpha case study.

...

Bay Street Hospitality is a diversified hotel fund series for allocators seeking quant-driven exposure across top countries, operators, and hotel tiers. The fund targets a diversified portfolio in both high-growth emerging markets and stable developed markets, optimizing risk-adjusted returns. The leadership provides structured equity and pivotal strategic guidance to hotel-related investments. The fund establishes joint ventures with best-in-class partners, focusing on deal flexibility, currency considerations, tax efficiency, and clear exit strategies.