Bay Street’s Phase 13 Regime Detection classifies European hotel and branded residence assets in 2025 as being in a “Capital Preservation Regime” for Asian investors.

In Bay Street’s private meetings with art families in Singapore, Hong Kong, and Abu Dhabi, we’ve observed a parallel interest: using European hospitality assets as cultural stages.

One collector of Southeast Asian modernist works recently told us in Paris:

“Europe gives our collections context. Guests here don’t just look; they ask questions. That’s the cultural dividend we’re paying for.”

This sentiment echoes Art Collecting Today:

“Collectors no longer seek passive display; they seek immersive environments where art is part of the lived experience.”

For Asian investors, branded residences and boutique hotels with licensed art programs provide more than cash flow; they deliver reputational alpha and reinforce long-term brand narratives back home.

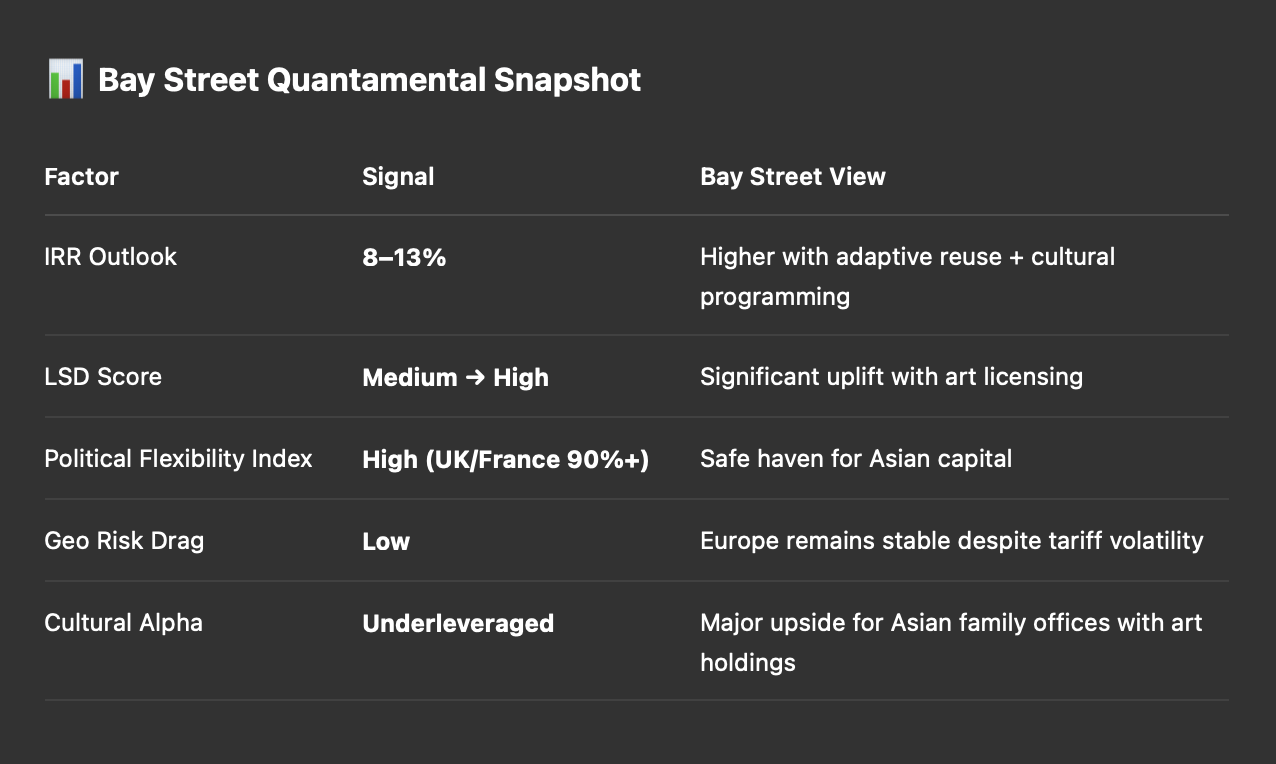

Bay Street’s models show:

Asian investors are not just buying European hotels for yield — they are buying a stage for their stories.

As Management of Art Galleries reminds us:

“The venues that endure are those that let culture compound.”

For Bay Street, the investment thesis is clear: The next wave of Asian capital will gravitate toward hospitality assets that merge financial defensibility with cultural resonance — making branded residences and boutique luxury hotels in Europe some of the most strategic plays for the coming decade.

...

Bay Street Hospitality is a diversified hotel fund series for allocators seeking quant-driven exposure across top countries, operators, and hotel tiers. The fund targets a diversified portfolio in both high-growth emerging markets and stable developed markets, optimizing risk-adjusted returns. The leadership provides structured equity and pivotal strategic guidance to hotel-related investments. The fund establishes joint ventures with best-in-class partners, focusing on deal flexibility, currency considerations, tax efficiency, and clear exit strategies.