Hi! Please leave us your message or call us at 510-858-1921

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form

6

May

Quantamental Hospitality Metrics: Bay Score, AHA, BAS for Public & Private Market Comparison

Last Updated

I

May 6, 2025

Executive Summary

This whitepaper defines the three core proprietary metrics that anchor Bay Street Hospitality’s investment strategy: Bay Score, Adjusted Hospitality Alpha (AHA), and Bay Adjusted Sharpe (BAS). These metrics are used to evaluate both private and public hospitality-related investments in a standardized, cross-comparable manner. Unlike traditional valuation and risk metrics, this framework accounts for deal lifecycle positioning, liquidity differentials, regional and sponsor risk, and strategic context. It empowers allocators to interpret opportunities through a unified scoring architecture designed to identify mispricing, quantify return potential, and benchmark portfolio decisions with institutional discipline.

I. Introduction

In the fragmented world of hospitality investing—where deal structures, geographies, and operators vary widely—establishing a consistent evaluation framework is critical. Bay Street Hospitality’s quantamental methodology integrates quantitative rigor with strategic context. At the heart of this approach are three proprietary metrics:

What is Bay Score? A composite measure of investment attractiveness, combining financial, structural, and strategic attributes into one unified score. Inputs that are inferred from CoStar submarket-level forecasting—such as RevPAR, occupancy, and volatility—are flagged with CoStar Method Tags and scored for Forecast Confidence (Low, Moderate, High) based on STR sufficiency and CoStar depth.

How AHA Quantifies Alpha? As a customized excess return calculation that adjusts for illiquidity and regional benchmark misalignments. AHA is updated quarterly using Time-Weighted Return (TWR) logic, aligned with NCREIF/NCREIF ODCE drift modeling.

BAS and the Benchmark Adjustment System: A risk-adjusted performance measure specifically calibrated to the unique volatility dynamics of hospitality assets.

Why These Metrics Matter to Allocators?

These tools were designed to bridge the informational gaps across private data rooms, public equity screens, and cross-border investments—so that every opportunity can be viewed through a single, quantitative lens with transparent assumptions.

II. Methodology

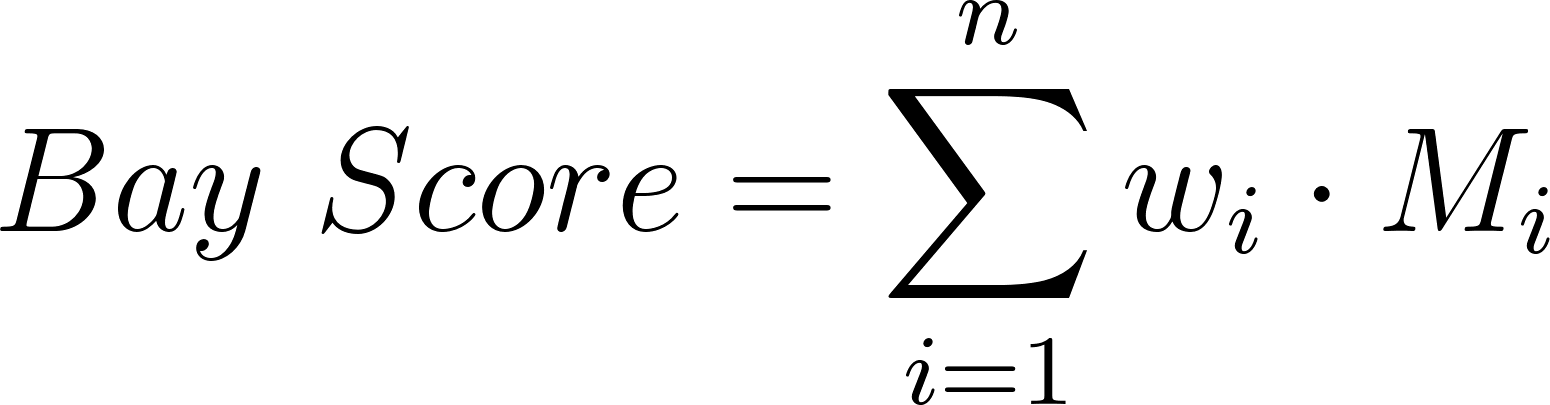

Bay Score: Composite Investment Attractiveness

Formula:

Where:

AHA = Adjusted Hospitality Alpha

BAS = Bay Adjusted Sharpe

R = Region Risk Score

F = Financial Stability Score

S = Sponsor Quality Score

L = Liquidity Access Score

M = Market Structure Score

wi = Weightings assigned based on proprietary calibration

Each sub-score is normalized on a 0–1 or 0–100 scale depending on the axis and derived through proprietary scoring sheets embedded in Bay Street’s evaluation app.

Adjusted Hospitality Alpha (AHA)

Formula:

AHA = Return − Benchmark − Illiquidity Premium, where the premium is modeled as a range (1–7.5%) based on LSD, FX volatility, capital lock-up duration, and repatriation risk.

This metric isolates true alpha by adjusting for the implicit premium investors require for illiquid or off-market opportunities.

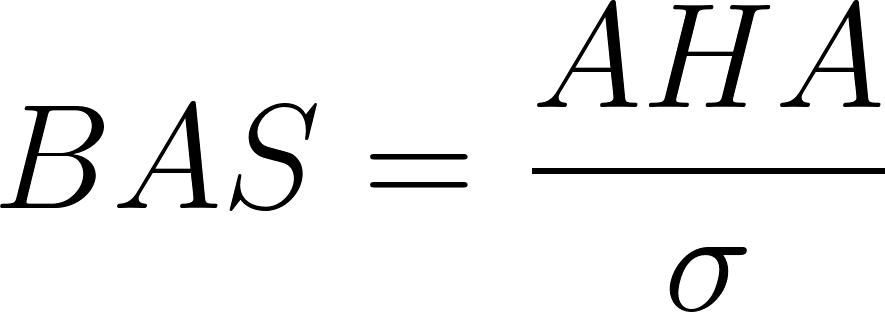

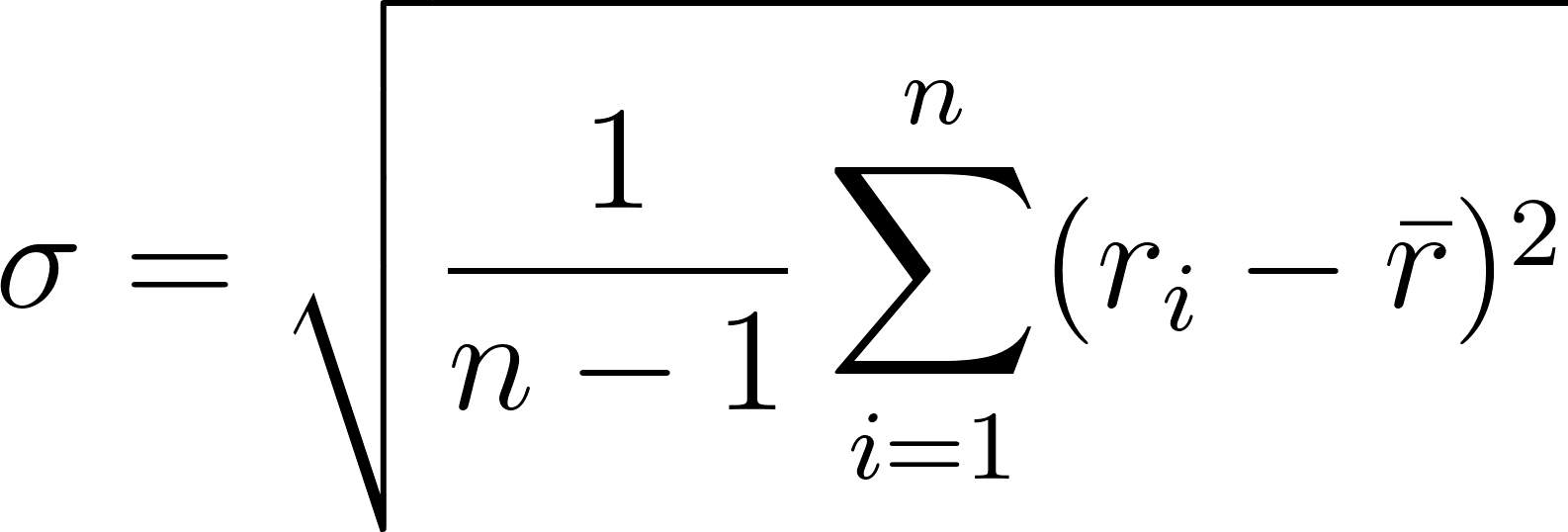

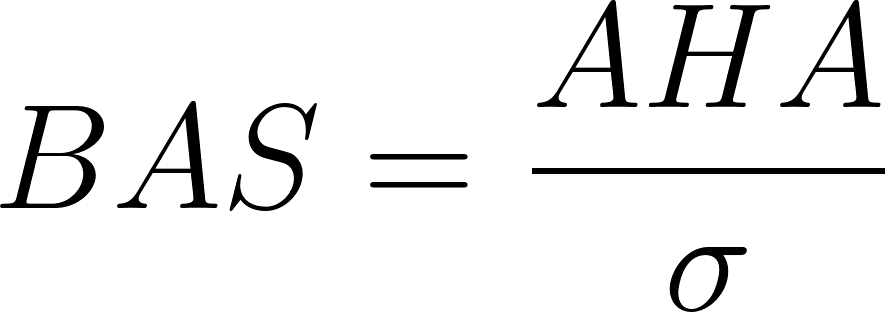

Bay Adjusted Sharpe (BAS)

Formula:

Where:

σ = standard deviation of expected returns (volatility)

BAS reframes the traditional Sharpe ratio by using AHA as the numerator, reflecting hospitality-specific excess return rather than generic risk-free spreads.

III. Use Cases & Applications

Deal Screening

Rapid scoring of inbound private data rooms to identify mispriced assets

Public equity screeners filtered by BAS to detect relative value

Regionally adjusted Bay Score outputs for global capital allocation

Cross-Asset Comparison

Use AHA to compare IRR-based private deals against public REITs or hotel operators

Normalize BAS across markets with differing volatilities (e.g., India vs. U.S.)

Lifecycle Adjustment

Apply forward-adjusted Bay Scores to pre-stabilized developments

Use trailing AHA for asset-managed stabilized properties

Adjust liquidity inputs dynamically based on fund exit window

IV. Quantamental Advantage

The proprietary metric set gives Bay Street Hospitality several core advantages:

Cross-Comparability: Whether a 4-star Lisbon hotel developer or a U.S.-listed REIT, all deals are evaluated under the same quant framework.

Real-Time Scoring: Plug-and-play architecture allows auto-calculation from raw inputs (data room or screener).

Institutional Rigor: LPs can trust that every deal undergoes systematic, repeatable diligence using quant-driven metrics.

Benchmark Integration: With ties to the Bay Street Hospitality Index (BSHI), all alpha is grounded in a real asset-class benchmark.

V. LP Takeaways

Clarity Over Complexity: Bay Score transforms fragmented data into a single number that guides investment decisions across public and private markets.

Alpha, Defined Differently: AHA anchors excess return not just to a benchmark, but to the nuances of hospitality investing—including exit liquidity and regional beta.

Risk-Reward That Matters: BAS shows whether the return is worth the volatility, using relevant hospitality-specific risk factors.

Global Perspective, Localized Precision: Regional inputs ensure Bay Score adapts to market nuance without sacrificing consistency.

VI. Appendix: Formulas & Benchmarks

Formulas Recap

Bay Score

or

AHA

AHA = Return − Benchmark − Illiquidity Premium, where the premium is modeled as a range (1–7.5%) based on LSD, FX volatility, capital lock-up duration, and repatriation risk.

BAS

IRR Proxy (for public assets)

Bay Street Hospitality Index (BSHI)

The composite benchmark is derived from an equally weighted blend of:

STR Global RevPAR indices

CoStar hospitality data

Cambridge Associates Private Hospitality

NCREIF Hotel Index

FTSE Nareit Lodging Index

MSCI GPFI Hotel Composite

S&P Global Hotel & Resorts Index

Dynamic Illiquidity Premium: A range-based premium (1–7.5%) applied to reflect liquidity risk, modeled using hold duration, FX volatility, repatriation constraints, and LSD scoring.

VII. Benchmark Methodology Integration

The Bay Street Hospitality Index (BSHI) integrates methodologies from leading industry benchmarks to ensure accurate and consistent performance measurement across public and private hospitality investments. Key integrations include:

STR Global RevPAR Index: Adopts the total-room-inventory (TRI) methodology for comprehensive room availability assessment.

NCREIF Hotel Index: Utilizes time-weighted return calculations for private real estate performance measurement.

Cambridge Associates Private Hospitality Index: Sources data directly from institutional-quality fund financial statements for private investment benchmarking.

FTSE Nareit Lodging Index: Applies free-float market cap-weighted methodology with liquidity and tradability screens for public REITs.

MSCI GPFI Hotel Composite: Implements time-weighted return methodology for property fund performance consistency.

S&P Global Hotels Index: Incorporates GICS methodology for classification and weighting of hospitality equities.

Dynamic Illiquidity Premium: Replaces static CPI + 5% with a range-based premium informed by LSD, FX risk, and market access friction. Reflects differentiated liquidity realities across asset types and regions.

These integrations ensure that the BSHI provides a robust, transparent, and industry-aligned framework for evaluating hospitality investments.

VIII. CoStar Methodology Integration & Forecast Notes

Bay Street Hospitality integrates CoStar’s hotel data and forecasting models throughout its quantamental platform. The following standards apply across all scoring, benchmarking, and projection tools:

CoStar Method Tag: Any value inferred from asset-level or market-level data using weighted submarket logic (e.g., ADR, occupancy, volatility) is flagged as modeled. These values follow STR sufficiency protocols and preserve contributor confidentiality.

Forecast Confidence Score: Each forecasted variable is graded as low, moderate, or high confidence, based on the density and quality of underlying STR data, CoStar submarket class availability, and alignment with Oxford Economics macro inputs.

Bay Score Trajectory Forecasts: Investment scoring visuals (e.g., for LP memos or dashboards) incorporate CoStar’s forecasting engine and display projected Bay Score bands under base, bull, and bear scenarios—anchoring underwriting expectations to institutional models.

These integrations ensure Bay Street Hospitality’s public-private benchmarking system remains accurate, repeatable, and institutional in nature.

IX. Copyright Notice and Legal Disclaimer

The materials provided by Bay Street Hospitality Fund I GP LLC (“Bay Street Hospitality”), including but not limited to the Bay Street Quantamental Strategy, Bay Street Terminal, Bay Street Hospitality Index (BSHI), Bay Score, Adjusted Hospitality Alpha (AHA), Bay Adjusted Sharpe (BAS), BMRI, and all related whitepapers, publications, presentations, and models, are for informational purposes only.

They do not constitute investment advice, an offer, or a solicitation to buy or sell any security, real estate asset, financial product, or investment strategy. The information herein reflects current opinions and assumptions as of the date of publication and is subject to change without notice.

No representation is made that any strategy, model, or methodology described will achieve any specific investment results or objectives. Past performance is not necessarily indicative of future results.

Certain data may have been obtained from third-party sources believed to be reliable; however, Bay Street Hospitality makes no guarantee as to its accuracy or completeness.

Unauthorized reproduction, distribution, dissemination, or use of these materials in whole or in part is strictly prohibited.

The July 2025 article by Andrew McGregor, VP Accommodation at Access Hospitality, opens a compelling chapter in the broader AI-hospitality discourse—one that Bay Street has been watching closely as it intersects with our cultural alpha thesis and the next layer of yield differentiation across the sector. McGregor doesn’t just call for better digital tools; he asserts a philosophical reordering of the guest journey itself. What we find most consequential from a quantamental perspective is how agentic AI—software that not only responds but acts—redefines not just conversion funnels, but the expectations of travelers shaped by Uberized decision trees, smart defaults, and context-aware prompts.

Philippe Ziade’s vision for AI-powered hospitality, as demonstrated through his Otonomus Hotel concept, underscores a broader truth Bay Street has been tracking: the next generation of hospitality alpha won’t come from bricks and mortar alone. It will come from the convergence of predictive technology and cultural narrative. AI promises to redefine operational efficiency, staff empowerment, and guest personalization, but the key question for investors is whether it can also defend yield and loyalty premiums in an increasingly competitive luxury landscape.

Asian investors are rediscovering Europe, and this time, the story is less about opportunistic portfolio flips and more about wealth preservation, yield diversification, and cultural brand-building. The trend, highlighted in the recent IHIF EMEA panel, mirrors Bay Street’s own discussions with Asian family offices and art dynasties seeking not just financial returns, but narrative defensibility — a theme that resonates deeply with our quantamental scoring framework.