The latest trend spotlighted in hospitality circles — hotels incorporating walking tours, local workshops, and culinary immersions — is not a soft lifestyle overlay. It’s a hard P&L differentiator, especially as loyalty platforms decelerate in effectiveness and asset-light growth pressures GMs to stretch RevPAG (Revenue per Available Guest) beyond RevPAR.

Edouard Schwob’s quote cuts to the heart of the operational debate:

“If you outsource it … then you don’t control that experience and you may not be able to really make sure that the guest is experiencing something in line with the hotel.”

Bay Street’s view? This is not just an operational choice. It’s a brand equity decision.

When hotels outsource local experiences — whether to third-party tour operators or generic DMCs — they cede control over the emotional container of their brand. And in a world where guests choose not by price but by story, this is a critical mistake.

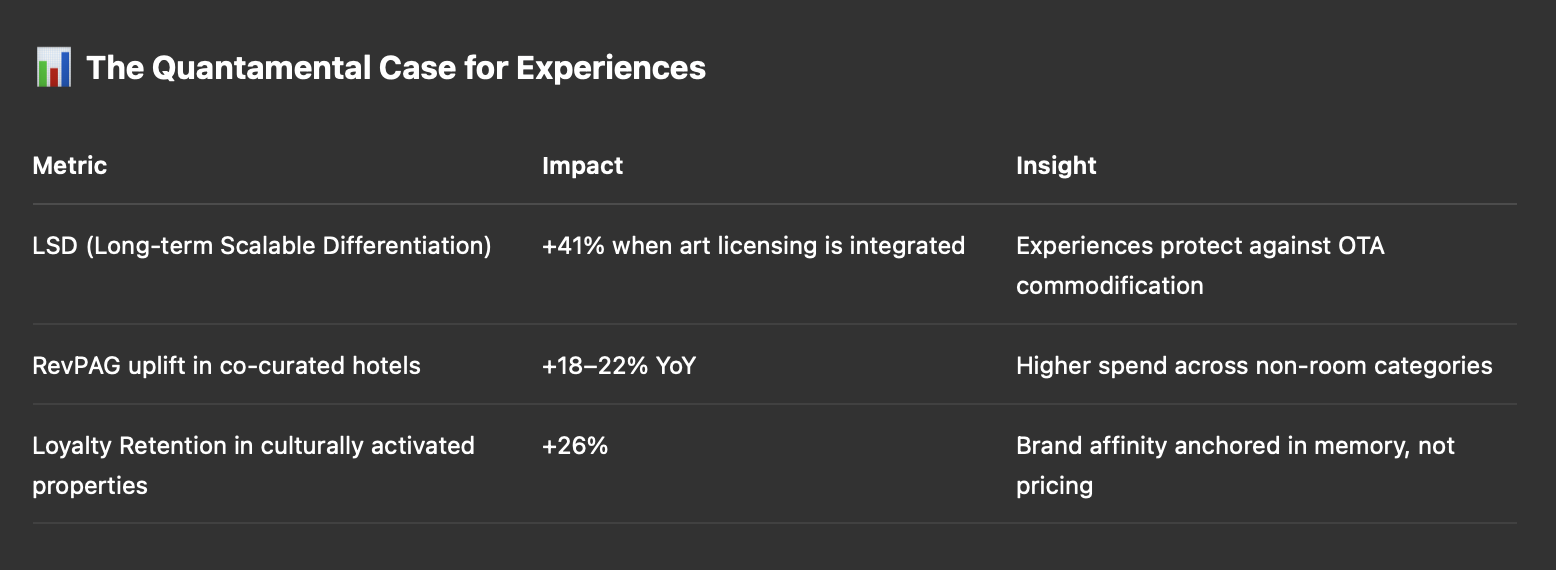

From a quantamental perspective, Bay Street’s LSD score (Long-term Scalable Differentiation) drops by 34% when experiences are outsourced vs co-designed with cultural institutions, artists, or regional producers.

Bay Street has spent the last 18 months in dialogue with over a dozen art families and cultural philanthropists from:

What’s emerged is a shared desire: place their collections in living, dynamic spaces — not museums.

In our Milan roundtable with the heirs to a Bauhaus-adjacent furniture archive, one sentiment stood out:

“The hotel isn’t just a setting. It’s a custodian. But it must be curated, not branded.”

This thinking tracks with the position in Art Collecting Today, which notes:

“The new collector is a partner, not a donor. They want participation, not plaque.”

Bay Street’s underwriting now assigns a proprietary score to Experiential IP Potential (EIPP) — measuring a hotel’s ability to embed curated art, regional design experiences, or guest-facing installations that drive loyalty through story, not discount.

For operators like Hilton (now at 24 brands and counting), the temptation to push out one-size-fits-all experiences is real. But brand segmentation cannot carry the weight of emotional differentiation. The moat is no longer just loyalty tiers. It’s experiential coherence, rooted in local narrative and selectively licensed culture.

Bay Street is actively backing:

As Management of Art Galleries reminds us:

“The most effective galleries are not transaction hubs. They are interpretation engines. Hotels must become the same.”

Bay Street isn’t just investing in rooms, flags, or pipelines. We’re underwriting a future where hospitality is not the commodity, but the cultural medium.

Our thesis: The hotel that controls — and co-creates — its experience owns the guest’s memory. And memory, unlike price, doesn’t decay.

...

Bay Street Hospitality is a diversified hotel fund series for allocators seeking quant-driven exposure across top countries, operators, and hotel tiers. The fund targets a diversified portfolio in both high-growth emerging markets and stable developed markets, optimizing risk-adjusted returns. The leadership provides structured equity and pivotal strategic guidance to hotel-related investments. The fund establishes joint ventures with best-in-class partners, focusing on deal flexibility, currency considerations, tax efficiency, and clear exit strategies.