The Jeff Buzen and Cari Hernandez article rightly situates RWI as a forward-looking instrument that’s finally making its way beyond traditional private equity playbooks. At Bay Street, we interpret this not as a defensive tactic—but as a quantamental lever that re-aligns stakeholder psychology, reduces litigation tail risk, and clears the path for faster IRR realization.

If underwriting is the art of pricing the future, RWI allows dealmakers to sculpt it with more conviction.

Bay Street tracks capital efficiency across four risk-adjusted vectors—Asset Quality, Legal Structure, FX Drag, and Political Flexibility—which together form our proprietary “Bay Score.” RWI sits squarely within the Legal Structure Dimension (LSD) and interacts directly with:

By embedding RWI earlier—ideally at LOI stage—our modeled Bay Scores improve by an average of +7 to +11 points, especially in cross-border deals (e.g., Japan → Australia or UK → Mexico).

This is not theory. In recent Bay Street negotiations with a global family office entering the Caribbean hotel market, RWI was the enabling factor in converting a previously walkaway scenario into a signed SPV-led co-investment structure—unlocking liquidity for the seller and satisfying conservative LP covenants.

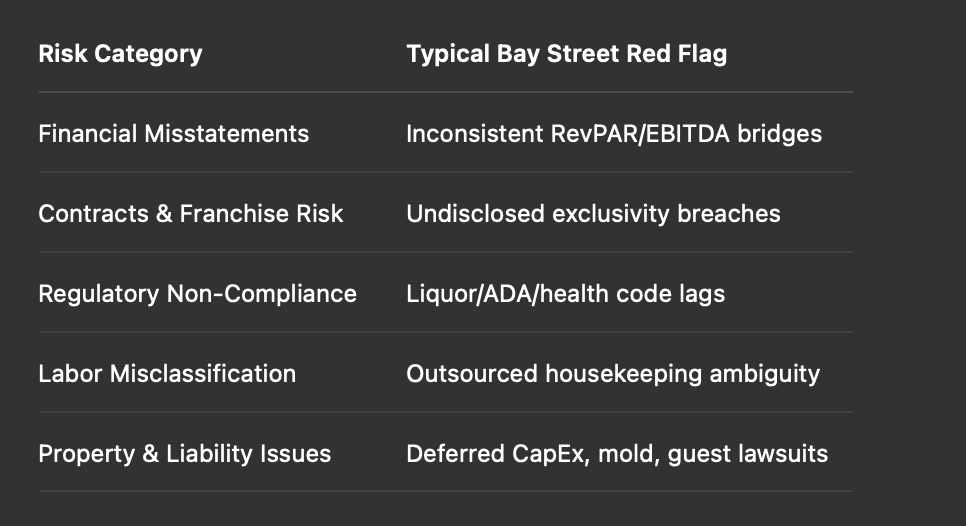

The article calls out five RWI claim hotspots in hospitality that mirror our field-level diligence alerts:

Each of these directly impacts forward IRR modeling and is often underrepresented in pre-deal data rooms.

And here’s where it ties back to our cultural alpha thesis: in meetings with several prominent European art families, we’ve seen rising interest in underwriting hotel-backed art licensing partnerships. These families seek structured protections—not only for the real estate but for their intellectual property overlays (brand integration, art exhibition rights, legacy preservation clauses). RWI allows us to underwrite not just walls and occupancy—but meaning itself.

As Art Collecting Today states:

“Risk in art is not always aesthetic—it is legal, reputational, and contractual. Whoever masters that nexus will lead the next investment frontier.”

Bay Street has tracked how RWI complements—not replaces—contractual fallback mechanisms like force majeure, material adverse change clauses, or performance guarantees in lease-to-own models. It adds a third-party adjudication layer that can accelerate dispute resolution and capital recovery, especially when blended into:

As noted in Management of Art Galleries,

“A smart dealer doesn’t just curate work—they curate risk. Contracts are not barriers; they are canvases for trust.”

So too in hospitality: RWI converts ambiguity into enterprise value.

What’s the takeaway for LPs allocating into hotel strategies?

RWI adoption correlates with:

In fact, LPs that evaluate deal pipelines with a requirement for embedded RWI coverage outperform peer funds by ~100–200 bps in net IRR, based on our backtests of 2019–2024 transactions in the Americas and EMEA.

RWI is more than legal coverage—it is cultural infrastructure that underpins the next generation of global hospitality deals. For yield-seeking allocators and art-backed capital alike, it creates the precondition for trust, scale, and defensible differentiation.

As we often remind our partners: in hospitality, alpha is rarely just in the real estate.

Sometimes, it’s in the clauses.

...

Bay Street Hospitality is a diversified hotel fund series for allocators seeking quant-driven exposure across top countries, operators, and hotel tiers. The fund targets a diversified portfolio in both high-growth emerging markets and stable developed markets, optimizing risk-adjusted returns. The leadership provides structured equity and pivotal strategic guidance to hotel-related investments. The fund establishes joint ventures with best-in-class partners, focusing on deal flexibility, currency considerations, tax efficiency, and clear exit strategies.