According to Savills, branded residences are projected to grow by 100% over the next seven years. Bay Street’s Phase 13 Regime Detection classifies this growth as part of a “Brand Extension Regime”, which carries both upside and risk:

The challenge, therefore, is narrative consistency — a brand must speak authentically to each demographic while maintaining its core identity.

At Bay Street, we see cultural programming as the untapped lever to defend yield in these blended residential formats.

In our recent meetings with prominent art families in London, Oslo, and Singapore, one recurring theme emerged:

“We’re not licensing art to decorate; we’re licensing to anchor a lifestyle.”

A third-generation collector of British modernist works noted:

“Co-living and wellness spaces need cultural gravity. Without it, they’re just rentals with branding.”

This aligns with Art Collecting Today:

“The new collector is a partner in the experience economy, and brands that provide that experience secure longer-term patronage.”

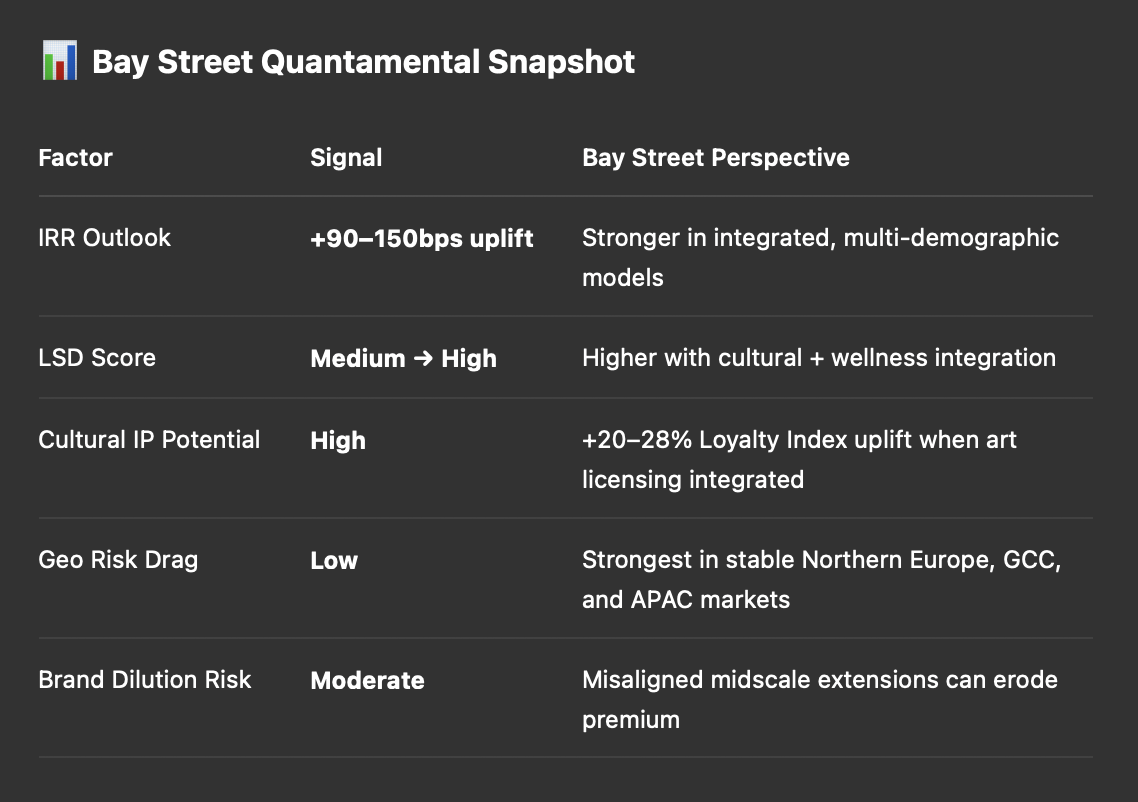

Bay Street’s models back this up: branded residences incorporating curated art partnerships show a +20–28% Loyalty Index uplift and higher RevPAG elasticity, particularly in wellness-focused or senior-living integrated models.

Bay Street views these as proof points that the highest-performing branded residences of the next decade will be mixed-use ecosystems with cultural IP woven in.

Branded residences are no longer just about hotel-style services; they are about anchoring lifestyle ecosystems. Those that integrate cultural programming, wellness, and co-living authentically will command loyalty and exit multiples well beyond traditional residential plays.

As Management of Art Galleries reminds us:

“Sustainability of cultural spaces comes from being a living system, not just a static asset.”

For Bay Street, the investment thesis is clear: Back operators who can run these branded residence platforms as cultural operating systems, not just real estate portfolios.

...

Bay Street Hospitality is a diversified hotel fund series for allocators seeking quant-driven exposure across top countries, operators, and hotel tiers. The fund targets a diversified portfolio in both high-growth emerging markets and stable developed markets, optimizing risk-adjusted returns. The leadership provides structured equity and pivotal strategic guidance to hotel-related investments. The fund establishes joint ventures with best-in-class partners, focusing on deal flexibility, currency considerations, tax efficiency, and clear exit strategies.