Choice’s revised 2025 guidance — now forecasting domestic RevPAR to range between –3% and flat — is less about sudden demand collapse and more about structural category exposure. Weak government travel and tepid international inbound flows are partially to blame, but so too is the brand’s historical orientation around midscale and lower-end assets tethered to U.S. consumer mobility.

Enter Canada.

Choice’s acquisition of the remaining 50% stake in Choice Hotels Canada from InnVest for $112M isn’t just a cleanup of legacy JV paperwork — it’s an infrastructural repositioning. As CEO Patrick Pacious explained, consolidating the Canadian portfolio (350 hotels, 30,000 rooms) under a direct franchising model enables not only full tech stack integration, but a platform to introduce Choice’s newer brands — particularly Cambria and extended-stay formats — in a market where brand fragmentation is still relatively high.

Bay Street has long argued that direct franchising, when paired with a regionally embedded team and harmonized asset management, creates brand control loops that are often undervalued by equity markets. This mirrors the lessons we’ve drawn from our recent meetings with art-family offices in Toronto and Montreal who are looking to license heritage collections exclusively with operating partners that own or control the full guest experience, not just the contract.

As Art Collecting Today notes, “Ownership of narrative requires ownership of channel.” We see the Canadian move as a similar narrative pivot.

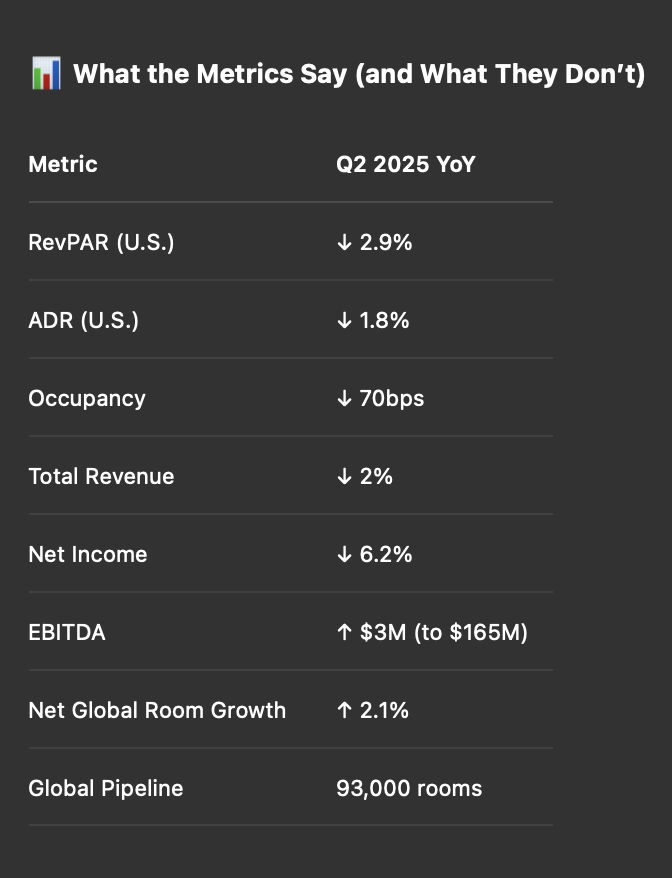

The drop in ADR (–1.8%) and occupancy (–70bps) would typically signal troubling demand elasticity. However, as Pacious highlighted, Choice franchisees are prioritizing occupancy share — a contrarian but strategically sound approach in a limited-service world where fixed costs scale slower than rate volatility.

This occupancy-stabilization tactic should not be misread as price weakness. Instead, Bay Street interprets this as a pre-positioning maneuver: preserving guest flow to set the stage for rate recapture when macro tailwinds return. It also plays to the resilience of the extended-stay model, where length-of-stay economics yield lower cost-per-occupied-room (CPOR) while preserving revenue intensity.

In Bay Street’s own language: they’re trading AHA (Average Historical ADR) for LSD (Long-Stay Duration), which — when coupled with modest FX drag insulation — keeps the Bay Score surprisingly intact.

With the Canadian deal finalized, Choice now operates more of its international portfolio through direct franchising rather than master franchise agreements. Why does that matter?

Because it shortens the feedback loop between brand experimentation and market reaction.

In Germany — where we’re watching hybrid leases evolve under slow regulatory liberalization — a similar trend is taking root. Our conversations with art families in Cologne and Düsseldorf highlight a desire for partners who can prototype guest-facing design interventions without waiting for franchisor approval. For art licensing to function as an alpha source, brand sovereignty is a prerequisite.

As Management of Art Galleries observes: “Brand latitude is not a luxury; it is a requirement for context-sensitive curation.” So too in hospitality franchising.

What investors often miss in midscale and limited-service models is how they echo consumer behavior trends in other cultural industries. Art licensing families understand this deeply: as the gallery world moves toward hybrid retail-exhibition formats, so too does hospitality shift toward extended-stay and flexible pricing formats that better reflect “embedded use” rather than transient luxury.

As we heard during a recent licensing strategy session in partnership with Bay Street’s curatorial team: “We want our collection to live where people work, not where they escape to.”

In that spirit, Bay Street sees Choice’s ongoing repositioning as a long game — not about chasing luxury RevPAR spikes, but embedding resilient capital flows in sectors that mirror middle-income domestic travel patterns, infrastructure megatrends, and regional labor normalization.

Investors scanning this report for signs of distress are missing the plot. Choice’s short-term RevPAR dip is less signal and more cyclical background noise.

What matters — and what Bay Street’s Quantamental Terminal is actively modeling — is how consolidations like the Canada deal, adjustments to ADR elasticity strategies, and expanded brand control lay the groundwork for durable yield across cycles.

Franchised economy and midscale portfolios are not immune to macro shifts. But when managed well, they act as compounding assets — much like core art collections under thoughtful custodianship.

As we often say: it’s not just the yield, it’s the story that surrounds it.

—

For allocation memos, FX-adjusted model runs, or pipeline concentration heatmaps, reach out to the Bay Street Quantamental Desk.

...

Bay Street Hospitality is a diversified hotel fund series for allocators seeking quant-driven exposure across top countries, operators, and hotel tiers. The fund targets a diversified portfolio in both high-growth emerging markets and stable developed markets, optimizing risk-adjusted returns. The leadership provides structured equity and pivotal strategic guidance to hotel-related investments. The fund establishes joint ventures with best-in-class partners, focusing on deal flexibility, currency considerations, tax efficiency, and clear exit strategies.